You can use these tips for any loan but are most effective for student loans since they are are not as big as home loans but are burdensome nonetheless.

If you answer YES to even one of the below questions you can read on for some ideas to cut down your debt drastically:

- Your loan is preventing you from fulfilling your true potential through creative pursuits?

- If you lose your job today you cannot afford to pay your monthly EMI installment without borrowing from anyone or liquidating assets?

- You have expensive life events coming up in the near future? Ex: MBA, parents’ health, marriage, starting a business, house, child etc

- You are not comfortable paying student loan debt every month for the next 10 years while also handling such expensive life events?

- You understand that paying a lower EMI each month increases your overall debt over time?

STRATEGY #0 : Resolve to pay off your loan in the shortest time possible

Yes. This can be done. I’ve done it so can you. Ordinary people with ordinary jobs have done it before you. The ideas below will seem drastic but What you need is not a high income but a minor change in mindset. Just follow the aggressive strategies below which will have the surprise benefit of netting you higher savings/month once your loan is paid off

STRATEGY #1: Lower your interest rate: Take a loan from your Parents and pay them back (without fail!)

Most likely your parents co-signed for your education loan so they are already on the hook if you don’t pay back the bank. The current education loan interest rate is 13.5% while the interest income your parents get from a bank fixed deposit is 8.5% : a difference of 5%. So why not take a loan from your parents and pay them a 0.5% higher interest rate and lower your monthly EMI by a few thousand rupees. Win-Win for everyone assuming of-course you pay them back on-time every month without fail.

CAVEAT 1: I would not advise getting a loan from any other family member as it creates a debt of gratitude you cannot shake off for the rest of your life. You are indebted to your parents anyway 🙂

CAVEAT 2: Some banks might charge a pre-payment penalty. Use this loan prepayment calculator to figure out how much you would save in paying extra interest if you prepaid.

STRATEGY #2: Pay double your EMI every month & more

This is the only guaranteed way to get out of debt fast. Even if you cannot ask your parents for help like in #1 above, this is completely within your control. Use this Loan Tenure Calculator to see for yourself how paying double the EMI brings down your loan repayment period drastically.

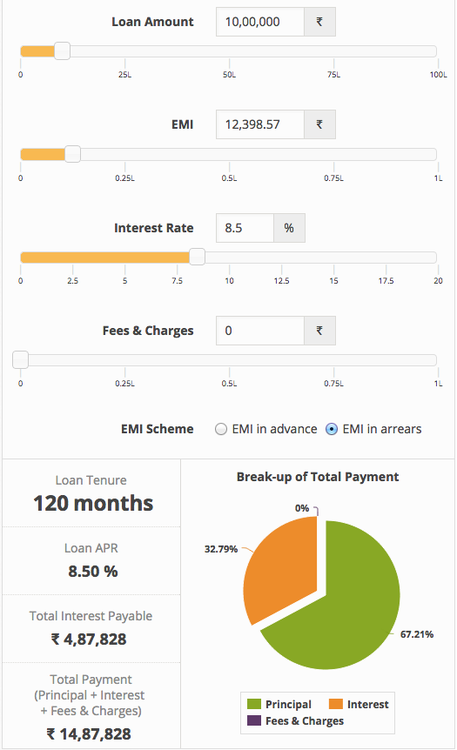

NORMAL EMI: Rs.10 lacs loan at 8.5% interest takes 10 years to pay off

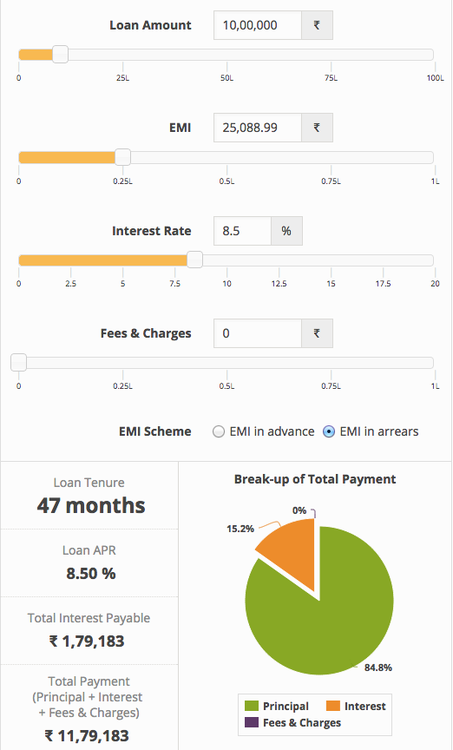

DOUBLE THE EMI: Loan repayment period reduces from 10 years to under 4 years!!!!

Where do I find money to pay more you ask? Well, first set aside double the EMI and live on only the rest of your take-home pay. That’s a bitter pill to swallow but read on for ways to help you put down double the EMI.

Pro-tip: Also plough your bonus, salary raise, birthday gifts, income tax refund etc all towards your loan payments dramatically reducing the loan repayment period.

CAVEAT : Some banks might charge a pre-payment penalty or paying more in EMI.

STRATEGY #3: Increase your surplus: Stop investing while you have debt

If you have debt at 13.5% then investing in any product that does not give a return more than 13.5% does not make sense. Till you pay off your loan, just invest in your employer’s mandatory EPF contribution because you get free matching contribution from your employer and maintain 6-12 months of emergency expenses should you lose your job

STRATEGY #4 : Increase your salary: Change jobs

Changing jobs is the #1 pro-active way to get a salary increase. Even if you don’t plan to change jobs, testing the job market will inform you what skills are valuable to keep yourself up-to-date should you lose your job and how much raise to ask for at your current job. Read this : Salary Negotiation: Make More Money, Be More Valued.

Pro-tip: If your job allows an overseas stint then push your boss hard to send you abroad so you can earn in dollars/euros and crush your debt in under a year.

STRATEGY #5: Increase your savings: Adopt a frugal lifestyle

I don’t want to sound preachy here but live lean & mean till you pay off your loan. Start by trimming the top 3 recurring costs in your monthly budget & plough the savings into you-know-where by now 🙂

- Rent (Makaan) : share a house with room-mates or stay with parents (if possible). Save money & time on commute by living close to your work

- Food (Roti) : Learn to cook simple items that you like & then pack them for lunch. Eating out is a real drain on savings. Online recipes are available galore.

- Clothes (Kapda) : Just get a few repeatable but smart formals for work and go with t-shirts/jeans till you pay off your loan

STRATEGY #6: Be smart: Take advantage of government & bank schemes

+ Women get a 0.5% interest rate concession. If you did not get this concession ask your loan-providing bank

+ Some banks offer a 1% interest rate concession if you pay interest promptly even when you were studying a.k.a moratorium period. So if you paid interest during college then check with your loan-providing bank to ask for the concession. See language from SBI bank

- 1% concession for full tenure of the loan, if interest is serviced promptly as and when applied during the moratorium period, including course duration.

+ Check if you are eligible for the Interest Subsidy scheme for low-income households where the government pays interest while you are studying. UPDATE: The option to file claims for past years seems to be closed now even though the scheme is operational for students. Online discussion

+ While filing taxes don’t forget to claim tax deduction on the interest paid. Less taxes you pay the more money on hand to pay more EMI. You can use ClearTax to file taxes online in 15 minutes

+ Take a term life insurance on yourself benefiting parents/spouse to protect them from your education loan debt after you. Twin benefits to this move: the insurance premium will not change in your lifetime AND is tax-deductible

[…] Read our blog post on how to pay student loan in shortest time. […]

[…] If you’ve bought a house on exorbitant EMI at an early age, you need to first crush your EMI. If you have education loan, learn how to crush education loan. […]

[…] have written a blog post on How to Pay off your Student Loan in the Shortest Time possible but it is applicable to all sorts of debt. Read it and you may find it very useful in reducing […]

[…] If you’ve made the mistake of buying a house on exorbitant EMI at an early age, you need to first crush your EMI or education loan (read my article on how to crush education loan). […]

[…] If you’ve made the mistake of buying a house on exorbitant EMI at an early age, you need to first crush your EMI or education loan (read my article on how to crush education loan). […]