If anyone asks you whether you will just idle away your time once you retire early in your 40s simply send them over to this list. Who knows maybe they’ll be inspired too!

I’ve optimised this list for personal happiness and focused on things you should be doing sooner than later before old age catches up and you realise you have less time & energy left to do the things that matter to you the most.

Top 10 things you can do in Early Retirement

You can pick one, two or all of them it is up to you now:-) as nothing is stopping you from living your dream life!!!

1. Spend more time with yourself

Pursue a hobby, learn to meditate, cook for your family, catch up on your sleep. Basically Figure out life at your own pace without having an obligation to work.

2. Spend more time with family

Especially if you have aging parents and young kids.

3. Work on your health and fitness

Almost all of us at some point or the other have compromised on our health while building our career. I did it. I pulled long hours at work, ate unhealthily and did not exercise. You can take this time to slowly work on building a healthy lifestyle by incorporating healthy eating habits and doing some form of exercise or sports regularly for ex: Yoga, Meditation, Swimming, Running etc.

4. Travel leisurely

Did you have a dream to travel slowly, absorbing a place by living like a local. Scratch that itch now by living in different places for a few months/years.

5 Work for passion

Almost all our adult life we worked mainly to pay bills. Now is the time you are free to pick any project for the passion of it. Earn money by only doing interesting work and refusing to do the aspects you did not like in your previous jobs.

6.Start your own business

If you always felt like being your own boss, try your hand at starting a lifestyle business to earn income doing something you like.

7.Volunteer your time at a non-profit

If lack of time was stopping you from helping a cause, go for it now! Volunteer your time at a non-profit of your choice or your kid’s parent-teacher association or the election campaign of someone you respect or mentor youngsters.

8 Go back to College to change your career

Maybe you always felt that you were working in the wrong field. Take this opportunity to go back to college to switch careers. You can even learn online these days to make a career change.

9 Go deeper in your spiritual or religious activities

A busy work schedule means less time to devote to soul-satisfying activities. With a more flexible schedule you can set aside more time for your spiritual & religious needs.

10. Take care of your finances

Work with a financial planner to ensure your investment goals, will, insurance etc are all on track. Help your old parents with their finances, health & retirement as needed.

Are you getting some more interesting ideas? Share them with us in the comments.

Working in isolation on your goals can sometime be lonely and demotivating. That is why we started our blog to share our story and form a community of like-minded people with a common goal of being Financially Independent and Retiring Early.

In addition to sharing our own F.I.R.E journey we also look forward to sharing the stories of our F.I.R.E readers on this blog.

This week we have the pleasure of a guest post from Anil, whose family has achieved 77% of their Early Retirement Corpus and is 4 years away from Financial Independence. Let’s find out how Anil and his family managed to achieve this in-spite of life’s ups and downs. Most importantly how they achieved their goal along with managing international travel alternate years and other household expenses (cook, maid etc).

Thank you Anil for sharing your journey candidly with all of us at Saving Habit (SH).

Q & A

Q1 SH: Tell us a little about yourself?

ANIL: I just turned the big 4-0 so I guess you can call me properly middle-aged. I’m a senior finance professional. Currently located in Pune and I really like it!

I’m married with a 3 year old daughter. Both my wife and I work though she’s just started working again after a 3 year break for the kid. Dad’s retired from a PSU job. Mom is a housewife. Neither my parents nor in-laws are dependents luckily.

My biggest influence is my dad. My grandfather died young and left him 3 sisters to get married and though I didn’t realize it at the time, he had to scrimp and save through most of my childhood to meet his responsibilities. When I think back about it, I realise that it left a huge impression on me – that money was never to be wasted, that it wasn’t so important to keep up with the flashy next door neighbor and that debt was always a crisis.

Q2 SH: What motivated you to work towards FIRE. Any trigger incident?

ANIL: Nothing very specific but it was during a point in my career about 5 years ago when I was generally unhappy with work, was working crazy hours because the team was short staffed and had some personal stuff going on as well. I was having fantasies about quitting and walking away and discovered the FIRE community – specifically Mr. Money Moustache. The whole idea felt like it was talking to me.

Q3 SH: What is your target age to achieve FIRE?

ANIL: I set it at 50 when I first started but have grown increasingly convinced I can get there at 45 – partly because I did my initial calculations wrong and partly because of the effect stock market increases in the last 4 to 5 years have had on my portfolio.

Q4 SH: What is your target corpus and how are you saving up for it ?

ANIL: My target is 25X my annual expenses, but I did keep a separate allocation for my daughter’s education and marriage. Old Indian habits I guess. I’m 77% of the way there. Hurray! My portfolio mix is:

40% equity (in Mutual Funds)

40% debt

20% PF, PPF (which I guess you can also call debt)

The skew towards debt is due to a history of investing illiteracy which I’ll talk about in the later question. I’m targeting 60-40 the other way and I figure I’ll get there in 3 years with a combination of ongoing SIPs and STPs.

I also own a debt-free apartment in Mumbai that I’m not counting because though I don’t stay in it, theoretically, it is my primary residence. In the future, if and when I do decide to buy a place to live in when I settle permanently, I’ll use this house to fund it (and hopefully have money left over to further buff up my retirement nest egg)

Q5 SH: What is your savings rate, any specific saving strategies?

ANIL: Let me first say that I have always been a saver. I bought my first car at the age of 31; if I ate out, I preferred cheaper options; not a device fanatic etc. etc, However, I was not always an investor. To explain, I’ll divide my saving/investment life into phases:

Early career (23-27): Decent salary but living with parents so no responsibilities and only real expenses were partying with friends. I was saving close to 70% of my salary. However, I was investing like an idiot. I took all sorts of ULIPs, applied for every IPO and did my tax savings mainly in PPF but also NSC.

Responsibility (27-31): My father retired. He had originally planned to settle in Hyderabad where he owned a house but suddenly decided to continue in Mumbai when he got a post-retirement job offer. We initially planned to rent but I impulsively decided to buy when we saw a house we liked. At the time, the loan EMI was 50% of my salary. Savings…except for tax savings stopped and all my money went towards the house. At the same time, I moved cities, got married so responsibilities increased. Excluding EMIs, my savings rate was probably 10%. Including them though, I was still at around 60%.

Accumulation (32-35): This was the phase when the money really started rolling in. I got a 4 year assignment in the US with a good salary. My wife was also working for 3 of those years. We were in a small town so didn’t have heavy expenses except for travel. We were saving about 50% of our combined salaries and since they were US salaries, it was a pretty good saving. However I was still really stupid about where the money was going. I had huge numbers sitting in my savings accounts in the US and even when I bothered to start FDs the interest rates were ridiculously low: 2% or so. I had some MF SIPs going on but compared to the overall savings I had, the amounts were too low to make a difference to the return

Working towards FI/RE (36-ongoing): Once I woke up to the whole concept, I started acting. Set my goals, made a financial plan, all my savings immediately were routed towards SIPs, got rid of my ULIPs, started STPs from my FDs etc. However, this coincided with some major life expenses – I had a kid, my wife took a 3 year career break to take care of our daughter, I relocated to India and a new city with associated expenses. My saving rate dipped but I’m proud that even through the worst of it, I still maintained a 25% savings rate and if I include PF 30%+. Now that my wife’s back working, we are back above 50%

Q6 SH: Who influenced you or people you follow?

ANIL: Mr.Money Mustache is the main one but as I got into it, I did follow a few others here and there. In India, it’s the usual suspects – Subramoney and Freefincal.

Q7 SH: How are you managing your saving rate with a young Kid?

ANIL: It’s not easy. I think the important thing is that we prioritise spending on what really matters to us. We send our kid to an expensive pre-school and daycare, we have lots of house help – maid, cook etc., we take foreign holiday alternate years but we have a cheap car, the rent from our Mumbai house covers the rent for our Pune house with a fair bit left over and we’re careful in other ways. In the end though, I’ll be honest and say that we both have high paying jobs and even with a fair bit of waste in our spending, we still manage a pretty high savings rate.

Q8 SH: You mentioned you were “ruthless” about a few things in order to reach your target?

ANIL: Between my wife and I, we had 2 lacs a year going towards ULIPs sold to us by family members. We closed them out accepting whatever loss there was. Took some gutsy decisions on moving largish FD money into MFs. Sold out all the little shares I owned from years ago wholesale without bothering to overanalyze. Essentially, I simplified my financial life. The main thing though is my ruthlessness in adhering to a budget. It is a generous enough budget and I am very careful in sticking to it on a monthly/quarterly basis.

Q9 SH: What are your plans after you achieve F.I.R.E?

ANIL: I definitely don’t want to completely kick back and relax. My goals are a little different. If I think about my career, it’s definitely been a case of the Peter Principle (for those who’re too young to know of it – the law is that everyone tends to get promoted to their level of incompetence). I was a great financial analyst so I kept getting promoted quickly and now I have reached a level where I hardly do any actual financial analysis…most of my time is spent managing people. Any job that pays what I now earn doesn’t allow me much scope to get my hands dirty. My main plan after I semi-retire is to try and find a job where I can accept a much lower pay in order to get back to doing what I enjoy with reasonable work hours.

Q10 SH: What is the one piece of advice you want to tell our readers based on your journey?

ANIL: I’m no expert and god knows I’ve made my share my mistakes on this journey but if I had to share just one piece of advice, it would be – “Start early”. Starting early made up for all the goof-ups I made over the years. Though I invested badly, the power of compounding covered up the errors and today I stand 4 years away from financial independence. I know I’ve been lucky in now having much responsibilities in those early years but I also made sacrifices – all my friends were buying cars – I used public transport to get to work; stayed with my parents; partied responsibly etc. That’s paying off now.

If anyone of you out there who has achieved or is close to achieving financial independence and wish to share your story on this blog with other readers. Please write to us on habit.of.saving@gmail.com. We love to hear from you.

The most difficult question to answer while planning for early retirement is- How much money I need to retire early? We have spent a fair amount of time thinking about the most optimal early retirement corpus number. In the end, we figured out the most straight- forward approach is to equate the retirement corpus to (X) times your annual expense. (X) being the number of years of expenses you want to save.

In this post, we will help you estimate how much money you need to retire early in India. This is a rough guideline that we have used to calculate our own early retirement corpus.

TABLE OF CONTENT

How much money do I need to retire early In India?

In this approach, the corpus you need is 1. Your INFLATION adjusted annual expenses (MULTIPLIED BY) No: of years of expenses, you want to save.

Step 1: Calculate your Inflation-adjusted annual expenses

Take your current annual expenses and adjust it for inflation depending on when you want to retire early.

For Eg: If you are age 30 and have an annual expense of 12 lakhs, and plan to retire by age 45, assuming an inflation rate of 6% you will need 28 lakhs in future value.

Current Age: 30

Current Annual Expenses: 12 lakhs

Retirement Age: 45: years to retire 45-30= 15 year.

Inflation: 6%

Annual Expense at the time of retirement= 12 lakhs * 6% inflation for 15 years= 28 lakhs per year.

Step 2: Establish how many years worth of expenses you want to save:

This is the most debated subject in the Early retirement community: How many years of expenses must be saved before hanging up your boots?

The conundrum is you save too less, you will exhaust your retirement corpus before you die. To save the fattest corpus possible- you need to work much longer. How to find the right amount to live happily on after you retire?

A blogger named Mr.MoneyMustache (MMM) is a rockstar in the F.I.R.E community for having confidently declared himself retired early at age 30 in the year 2005 to raise their young baby. 13 years later he is about 43 years old now. That is a lifetime in the F.I.R.E community and hence he is a role-model for Early Retirement.

He recommends an early retirement corpus of 25 times your annual expenses at the time of retirement, also referred to as 25X.

What is 25X based on

MMM says:

Take your annual spending, and multiply it by somewhere between 20 and 50. That’s your retirement number. If you use the number 25, you’re implicitly using a 4% Safe Withdrawal Rate, which is my own personal favorite number.

So where does this magic number come from? At the most basic level, you can think of it like this: imagine you have your ‘stash of retirement savings invested in stocks or other assets. They pay dividends and appreciate in price at a total rate of 7% per year, before inflation. Inflation eats 3% on average, leaving you with 4% to spend reliably, forever.

It is essential to understand how 4% safe withdrawal works. So we recommend you read the above post.

Our take on the 25X approach

There was once a naive time in the past when we believed this simplistic math because we desperately did not want to work in unhappy jobs ever again.

25X seemed like the shortest target we had to reach. But after coming across the following limitations, we’ve become a bit sceptical about the 25X target. And more conservative in our approach:

The Trinity Research Study quoted by the F.I.R.E community is a study done for traditional retirement. It shows that a retirement corpus will last for 30 years with a 4% safe withdrawal rate even if there are market downturns. But we are not aware of any such study done for Early Retirement which by definition lasts for more than 30 years throwing a big question mark on whether 25X alone is enough to retire early and live off for say 40-50 years.

Unforeseen old-age healthcare expenses and inflation in health insurance premium.

Broken public amenities in India require you to spend extra for private backups

As a result of the above reasons, we’ve changed our attitude towards this math, work and early retirement in general. It is better not to have a corpus that is “just enough for living expenses” dependent on unpredictable market returns.

Sooner you want to retire- more no: of years you will live on your retirement corpus and bigger it needs to be.

If you are rigid about not wanting to work again then go with the exact number you get after the above calculations.

But, If you are flexible and willing to do some part-time work to cover some part of your expenses you can quit the job with much less corpus. keep reading to know how.

Our Practical Approach : 25X Corpus + Active Income

Don’t worry if a corpus of 50X or 6 Crore by age 40 seems like a really large number!

If you are like us and want to use early retirement to make a career shift, start a business or even travel the world we recommend a more practical plan.

This approach balances your desire to live your life at the earliest and the hard truth that you need a safety net before embarking on that life. Here goes:

Age 30-45: Target 25X within 10-15 years to become financially independent first. This is very much achievable with a savings rate of 50%. Start early in your 20s if you can.

Age 45-50: With 25X of expenses as the safety net, you can afford to quit your job and figure out how to make money from your real interests in life. A new venture can take 3-4 years of focus before it starts covering your living expenses.

Age 50-65: Once your new venture succeeds, invest any surplus to grow the 25X to give yourself a really secure old-age retirement. You have another 15 years to grow the 25X into say 40-50X.

This approach allows you to pursue your passion early in life using a reasonable safety net of savings.

If the thought of “working” after Early Retirement puts you off, I recommend re-reading the section above on inflation in India that convinced us that working on something we like from a position of strength is better than running out of money and being forced to work from a position of weakness.

So yes! we recommend 25X corpus as the Early Retirement Target. but not to live off of it for the rest of your life. but to use it as a safety net for a few years when you make the leap into the unknown.

Most F.I.R.E aspirants don’t seem to recognize that their Life is passing them by as they try to build the largest corpus possible before quitting jobs they don’t like.

The downside of trying to save 50X in 10-15 years is that you have to earn a lot of money sacrificing your prime youth in the process. That is the opportunity cost of trying to build a huge “war chest” before taking even the first step towards your dream life.

To put it bluntly: If you don’t feel confident with 25X you may not feel confident even with 50X.

We are grateful to Mr.MoneyMustache for helping us understand that Early Retirement is possible with the help of reasonable savings, can-do attitude and some active income after retirement.

But his passionate followers make the mistake of assuming that his 25X corpus recommendation is the “maximum” corpus needed. When in fact it is the “minimum” needed to balance the opportunity cost of living the life you want versus slogging till age 60.

I’m quoting his exact words below to explain this better (I’ve bolded the most important sentence) :

… you don’t have to be insanely conservative, working for year after year to ensure a gigantic starting nest egg before daring to retire.

…Once you quit a full-time job, you just need a small positive savings rate to stick around and keep trickling into investments. This will automatically become a cash snowball as you go about your daily retired life. By the time you’re old enough to need it, it will be bigger than you can possibly need.

It is very comforting to read success stories of people, especially if you have a similar goal as them. We love to learn from the experiences of people who have already achieved Early Retirement. Today we will share 4 of our favorite Blogs on Early retirement with you. They are U.S centric blogs. Since the FIRE community is much older and active in the USA it is only obvious that some of most enriching blogs are from there.

You may find understanding the maths in these blogs bit tricky, because of different currency, social context and financial markets. But still there is a lot of knowledge in these blogs that we feel can help and motivate any FIRE aspirant.

MMM is a cult in himself and for a reason. He retired at age 30 from his job as software engineer in year 2005 to raise his baby boy. He talks about his finances and his lifestyle on his blog, since year 2011. He is now 43 and still going strong, famous for his badassity and redefining early retirement with a young family. He is married with one kid and lives in Colorado, USA.

Why we love MMM: His style is a mix of frugality, smart investing and DIY projects. He lives a pretty awesome lifestyle and on a closer look you will realize that he is much more than an Early retirement Guru. He is a life-optimizing machine- from grocery bills, to biking routes, to laundry frequency- he optimizes every aspect of his life and shares it all with his readers on his blog.His writing style is free, thought provoking and amusing at times when he refers to his targets as Car Clown, complainy-pants and consumer suckas.

What they do after Early Retirement: Mr. MMM spends time building things (renovating house, office building etc), sharing his story on his blog, bartering his skiils for a holiday in Hawaii and other stuff :-). And Mrs. MMM runs a successful 5 figure e-commerce shop.

Frugalwoods If you dream of retiring early to the woods- take a page from her. She retired to a homestead in Vermont USA. A queen of extreme frugality and a fine example of how one can live a fulfilling frugal life without endless compromise and achieve financial freedom. She makes frugality appear fun and a obvious way to live life. She is an author and a mother of two. On her blog Frugalwoods she writes about her monthly finances, living frugally, raising kids on a budget, life in a homestead and throws frugality challenges. She lives with her husband and two daughters in a homestead in Vermont, USA.

Why we love Frugalwoods: She makes frugality look possible, her perspective on using old/second-hand stuff from clothes to furniture is pretty convincing, and we love to read her posts on raising her beautiful family on budget.

What they do after Early Retirement: Frugalwoods writes on her blog, authored a book and had a second daughter after achieving financial independence. Her husband is a techie who works full time from their homestead.

One of our Favorite blog post by Frugalwoods: The Myth Of The Gross Used ThingsThough we may not bring ourselves to buy & wear used clothes from a thrift store, we agree with the rest of the stuff 🙂 Especially buying used furniture and hand-me-downs for kids from family and friends.

Joe retired at 38 from his engineering career to become a Stay At Home Dad. As he progressed in his career he realized that the job was not a right fit for him and he had to get out of there. He started a blog to share his journey and keep a tab on his progress while he was still working. He is unique in sharing the dilemma about his job and his exit strategy from the corporate world on his blog. He is married and has a son and they live in Portland, USA.

Why we love retireby40: Joe focuses and shares information on building a passive income through real estate, dividends, P2P lending etc.. He also shares daily challenges of a stay at home parent, raising a kid and managing monthly budget after early retirement.

What They Do After Retirement: Joe is a Stay AT Home DAD and a blogger. His wife works full time, but has a plan to join him in Early Retirement in the next 2 years.

Who does not dream of retiring early and traveling the world. That is exactly what GoCurryCracker are doing after quitting their hi-tech jobs. They retired in their 30’s to travel the world and travelled 29 countries in first 3 years. They felt there is more to life than a good job, buying a house & working for 30+ years. From the start they saved and invested a big part of their income to fuel their dream of financial independence and world travel. They stayed in smaller houses, used bike instead of owning the car, ate home cooked food and only bought what was needed to save money.

Why we love them: They write about a nomadic life on the road with a child and cost of living for each country they visit. We also love reading about how to travel for free.

What they do after Early Retirement: They travel 🙂 also, Winnie pursues photography and Jeremy writes on his blog Gocurrycracker.

Also we want to give a special mention to Earlyretirementextreme.He is among the first few to achieve and write about FIRE. We may not relate to his extreme saving and ultra simplistic lifestyle but have tremendous respect for his view on life and FIRE. If you have a minute more, do read his Manifesto.

That is all from us for now! In the weeks to come we will share the list of of our favorite bloggers in India.

Do share your favorite bloggers and why you like them with us in the comments. We love to hear from you.

F.I.R.E is an acronym for Financial Independence and Retiring Early. There are a lot of U.S bloggers who write about their F.I.R.E journey. Most of these blogs assume that the readers are already familiar with the concept. We’ve been on this journey in India for over 5 years and to be honest we find ourselves questioning the basics and math behind F.I.R.E every year because we don’t want wrong assumptions made in our 30s to affect our quality of life in old-age. Like for example:

Does F.I.R.E mean you no longer have to work ever again in your life?

But what if your money runs out before you die?

What about other unforeseen emergencies that cost a lot of money?

Will you regret quitting work when faced with such situations?

You get the drift….so we want to clarify this F.I.R.E concept to the best of our understanding.

In this blog post I will share what is the general understanding of F.I.R.E globally and where our family’s approach differs from the globally accepted approach. Please remember that this is a complex topic and it will take multiple blog posts to fully cover its complexities. Treat this post as a very basic primer and read the rest of our blog to fully understand the details.

TABLE OF CONTENT

What is Financial Independence and Retiring Early

F.I = Financial Independence. When you don’t depend on a job to meet your monthly expenses then you are financially independent. This is possible if you invest your savings in assets that generate a passive income equal to your monthly expenses. Assets like Real Estate, Stocks, Mutual Funds, Fixed Deposits etc. If your monthly expenses are Rs.1 lakh and you receive rental income of Rs.25K, interest income of Rs.25K and dividend income from stocks of Rs.50K then you are financially independent.

R.E = Retiring Early. If you achieve financial independence at an early age say in your 30s or 40s then you can declare yourself to have retired early. Typically people retire from active work at age 60. So if you have enough money to never work again in your 30s or 40s then you have achieved Early Retirement.

So the key difference is that once you are Financially Independent(F.I) you may decide to continue in your career but you may get picky about what kind of jobs you choose because you are no longer dependent solely on salary income. Example: You may decide to work for a startup to learn a lot in a short period of time so you can become senior management faster than at a corporate job. You don’t mind the risk of the startup going out of business because you are financially independent. You will also take tough decisions at work without caring about your monthly paycheck as you are no longer dependent on it.

With Retiring Early(R.E), you are planning to quit your current career altogether and branch out into other activities that you are passionate about. Example: working for a non-profit, traveling the world, taking care of family etc. Note that with Retiring Early the opportunities for earning money are much lower because you will be spending time and money in non-remunerative activities. Naturally if you plan to Retire Early and never work again you need a much larger corpus than if you were to be simply financially independent.

Why are they referred together as F.I.R.E

The reason it is called F.I.R.E is because the path for both is similar : Saving a large amount every month to reach your target as soon as possible via frugality and/or high income. Only difference is the target corpus needed and what you plan to do after you achieve it. Some people want to achieve F.I as a backup but they don’t want to quit working. Not all people hate their jobs.

Now the Retiring Early part is tricky because no one seems to have done it yet in the F.I.R.E community. By that I mean, no one has retired in their 30s or 40s and lived till age 90 by simply living off their saved-up corpus with no extra income and blogged about it for 50 years. That’s right! this concept is so new that it has not been tested in real-life yet.

Another important issue is that one person’s lifestyle might not be suited to another person. Are you willing to Retire Early to a village with no modern amenities? If not then your corpus amount needed will be significantly higher.

Philosophy of the Financial Independence and Retiring Early (F.I.R.E) Movement

But to condense it here I would say quest for F.I.R.E is based on maximising quality of life, happiness and work-life balance.

In that sense F.I.R.E is less about not having to work ever and more about having the freedom to pursue your dreams in life. It means that you can design your life without taking money into consideration.

At a more philosophical level F.I.R.E also forces you to look at another important life questions that only you can answer for yourself:

What would you do with your life if you didn’t have to work for money?

How much is your freedom is worth to you?

Once you achieve freedom through F.I.R.E what do you plan to do with your life?

Our Key observations on Financial Independence and Retiring Early (F.I.R.E) concept

There is a wealth of knowledge available on F.I.R.E online that helped us establish our understanding on this subject. However, mostly all the bloggers have their own personal touch to this concept and what they mean by F.I.R.E. Few things we noticed which are worth mentioning at the outset are:

1. F.I.R.E is still a nascent concept

It is still a nascent concept which attracts lot of controversy on its viability even in the U.S where a dozen people have already retired early and actively blog about how they are managing their expenses and investments after achieving F.I.R.E. So it will be interesting to see how all the theory pans out in real life in next 20-30 years. It looks promising but we feel it will not be without a few bumps on the way.

2. There are different flavours of F.I.R.E

There are so many variations of F.I.R.E that it is easy to get confused or dogmatic and hesitate to get started. For example:

1. Mini-retirement

If you are F.I you can afford take a break from working to take care of your old parents/young baby or travel the world and then join the workforce after a few years. Notice how this bends the definition of Financial Independence(F.I) I gave earlier.

2. Part-time retirement

You are R.E but you work as a consultant or freelancer only for certain months of the year say during tax season or you run an online store that you operate only during Diwali/Christmas season. This bends the definition of R.E I gave earlier.

3. Permanently Retired aka Never work again:

This is the holy grail that attracts most people to Early Retirement. I’ll discuss about the viability of this in my next blog post.

We recommend that you not waste time debating the “exact” definition but instead focus on your day-job and achieve Financial Independence first with 25 times annual expenses as the initial target while also figuring out a side-income based on your passion that can fund your expenses. This way you’ll have two layers of protection : side income and saved-up corpus. Plus since the side-income is based on your passion you might not feel like it is work.

3. Almost all F.I.R.E people we know have active income

Almost all the people we know who have achieved FI or RE have not stopped working for money completely. Some have taken time off to travel, raise a kid, or just explore life but all of them have figured out some passion that generates side income which not only covers their expenses but continues to add to their net worth. We find this approach smart and practical as you get your freedom to explore your life along with some side income to support your expenses fully/partially.

4. How viable is it in India

We are confident that the concept is solid and can be practiced in India. But not without major modifications to the core idea. The idea of this blog is to share what works for us in India and what does not. We will keep sharing our observations with you as we go about it.

What Financial Independence and Retiring Early (F.I.R.E) means to us

Financial independence offers us the freedom to pursue our life goals and dreams. Turns out we are in a unique situation where we are already doing that and saving up for F.I.R.E at the same time! Once we were debt-free, owned a house without loan, and had 7+ years worth of expenses we quit our jobs to pursue our dreams in Goa. 3 years into the business we are our own boss. Our business covers all our expenses (we still live frugally), we work on our own terms, and also have location independence. If we could reinvent ourselves with just 7 years of expenses saved up imagine what you could achieve with 25 years of expenses saved up.

Disclaimer: With 7 years of safety margin we did feel a certain pressure and insecurity about the future. In the first 3 years when the business did not cover our expenses fully we lived very frugally. But it did serve its purpose and now we want to increase that safety margin to 25X.

So, are you tempted to F.I.R.E too? Share you views in the comments below.

Feel free to ask us if you have any questions on this concept. We would love to answer them to the best of our ability.

Why should you be interested to be Financially Independent and Retire Early (F.I.R.E)? When my husband first introduced this concept to me I asked him the same question. why should I miss out on fun now for later?

I was in my late 20s and the future seemed rosy and under control. I did not immediately see the need for us to talk about our finances and investments so early on in our courtship. Also, statements like “save for a rainy day” or “save now for future” were something I was used to only hearing from my grandmother. I thought “Saving” is not a subject to discuss for us cool young people. No one was talking about saving, instead EVERYONE I knew was buying things on debt, banking on their future earning potential without any hesitation.

To me, debt and EMIs seemed a natural solution to all the future problems that Naren was talking about.

So you must think what changed so drastically that only after couple of years from our first conversation I am writing this blog post? trying to convince you how Financial Independence and early retirement can improve your life.

Actually, nothing drastic- I just had to scratch the surface of my life to see how in-spite of doing well in my job I could not see myself keeping the same pace at work forever, plus I missed the freedom and autonomy: I could not experiment much with my life, my bucket list was growing longer. How much can you do in 2 weeks holiday per year( not all of us are lucky enough to even take that).

For the first time in my adult life I could see that I can do something about most of these issues. And that is how slowly and gradually I became a FIRE convert :-). So, today I will share with you some compelling reasons to consider F.I.R.E as a solution to your problems as well:

TOP 5 REASONS TO BE FINANCIALLY INDEPENDENT AND RETIRE EARLY (F.I.R.E)

#1 Because why not

Resist the herd mentality. There are 1000’s of people who have done it and they share how they did it on their blogs just like us. Financial Independence and early retirement may not have been possible in India 30 years back because people did not have such high-paying private jobs, investing in the equity markets was not easy or trustworthy and F.I.R.E role models were almost nil. All that has changed now. The secret to achieving F.I.R.E in 10-20 years is very well-known now to anyone who wants it:

Save and invest atleast 50% of your income

Spend smart: saving a ton each month forces you to optimize your spending

Stay Debt-free : Save and buy even big-ticket items instead of taking a loan

Earnmore if you are not able to save more

Don’t feel pressured to follow the wasteful spending habits of your peers

#2 Freedom

I like being my own BOSS. Freedom is a very basic human need. In our personal life also we crave freedom in our work, in how we spend our personal time and in having freedom of speech. I personally wanted to just explore who I was and what made me happy when I quit my job. F.I.R.E gives an opportunity to be your own BOSS, to claim your freedom to explore your life and interests with confidence and security. It did for me! Take a few minutes, and imagine all the things you will do if you had freedom and time

#3 Courage and Peace of mind

Personally I perform really well in crisis and stressful work environments. But I also love peace and tranquility in my day-to-day life. Knowing that we have no debt + 1 year emergency fund stashed away and that we are on the road to F.I.R.E gives me a peace of mind in this ever chaotic and changing world. I feel prepared to handle any life crisis that life may throw our way with confidence. I know I have something solid to fall back on and it gives me tremendous courage and peace of mind. Should all of us not strive for it?

#4 Family Harmony

The fact is through out our lifecycle the ability to work (no: of hours) keeps changing. It is highest in 20s, as one usually has single-minded focus on career, has time and energy to pull overnighters and long working hours. But that gradually changes once you get married and you want to spend quality time with your spouse and fulfill other household and social obligations.

The biggest change in your ability to work (no of hours) happens after you have a baby. You need considerable amount of time, physical and mental energy to raise a baby. Then again you get your time back in your 40s when your kids are grown up and are independent and you again have more time to focus on your work.

Naren and I saw considerable decline in our work hours starting from the early days of our pregnancy: doctor’s appointments, health issues, prepping the house for baby, making big purchases and life decisions took considerable amount of time. Most of us live in a nuclear family and most often both the partners are working and also share equal responsibility towards household work and parenting. Our current work culture does not accommodate this fact of life. Especially in highly competitive careers where most of us are ambitious to do better in life.

In middle of big life changes such as Marriage and having a baby add in time crunch, massive EMIs, other debt, no emergency fund and you have a perfect recipe for personal stress and marital disharmony.

Knowing all this in your early 20s would you not like to plan your life so that you can avoid these pitfalls and be in a position of strength so that you can enjoy the most beautiful transitions in your life.

#5 F.I.R.E helps your money to work for you

Just making more and more money to fulfill your financial goals is not the smart answer. You may convince yourself that you deserve it, you work hard. But you also deserve stress-free life, quality time with you family, flexibility to take care of your aging parents and pursue your dreams. If you only depend on your income to meet all you financial goals you are missing out on maximizing on your hard earned money. Through FIRE we plan to create enough financial assets that they act like a third person earning for us 24X7. Money never stops working, never sleeps. So take advantage of this fact.

Through FIRE we plan to create enough financial assets that they act like a third person earning for us 24X7

#6 (Bonus) Environmental reasons

This is a BONUS reason. Last but not the least and a major motivator for me to retire early. Being a millennial I enjoy the countless consumer choices that life offers us in the 21st century. However I also feel a knot in my stomach to see how much we waste. When I compared my life to our parents generation I knew that I was consuming much more than I needed and I was not any happier for it. Our incessant need to upgrade our lifestyle, to treat ourselves to feel worth-it and keeping up with Jones’s makes us spend way more then we actually need to be happy in life.

F.I.R.E not only gives you freedom to live your life but also helps you live a more conscious and environmentally friendly life.

So, what are you waiting for! Share with us in comments what is your top most reason to be Financially Independent and Retire Early.

We are starting this series of hacking luxury on budget, where we will share how we enjoy luxury on budget. Saving up for the long term, being mindful about your spending and prudent with your money can sometimes make you feel like you are missing out on fun. So, we always keep our eyes and ears open for good deals and whenever opportunity arises we grab it and enjoy! Such breaks rejuvenate us and we come back even more energized towards our financial goals.

Life really is about balance and a little bit of luxury on budget provides us with the experiences and memories that fuel our consistency towards our financial goals.

Hack #1- Our 4-star hotel club membership

One such luxury we enjoy is our annual membership with a Four star property in our neighborhood for an annual cost of only INR. 6,000 (inclusive tax). We mainly got this membership for the pool access, it is a beautiful pool with a view of a river. But the best part is along with pool access, the membership offers us perks worth over INR. 20,000. Keep reading for a detailed break-up or watch the youtube video I made during our recent complimentary stay at the hotel.

Swimming Pool. picture: The Crown

Alfresco Dining By Pool. picture: The Crown

View from The Swimming Pool. picture: The Crown

Watch video of how we hacked one night stay at a 4-Star Boutique hotel with spa and meals for just INR 2,000

We pay INR 6,000 annually and get perks worth INR 23,000:

Swimming pool Access ( Value: Rs 9,600 / based on Public pool costs- 400 per person/month. The hotel pool is much cleaner & less crowded than a public pool)

One night complimentary stay (Value Rs. 8,000)

Cake on birthdays and anniversary ( Value Rs.1,500)

2 complimentary Spa Vouchers (Value Rs. 2,200)

2 Breakfast vouchers(Value Rs. 2,000)

THIS TOTALS TO INR 23,300 for which we pay only INR 6000.

Few other Perks we get as members:

20% off on spa % & food and Beverage at Hotel

4 Vouchers for 50% off on room night

2 vouchers- 2 Nights for the price of 1 certificate

2 vouchers- free upgrade to next category

2 vouchers- buy one get one free

20% discount on banquets hall

The CRISIS converted into a holiday:

So, here is what happened. We live on a ground floor, and our house was infested with ants for months. We tried all kinds of home remedies as well as ant repellent spray but nothing worked. In the end we had to hire a professional pest control agency. The agency asked us to vacate the house for minimum 3 hours after spray as inhaling the fumes can be harmful. But due to a health reason, we decided to leave our house for 24 hours after fumigation just to be safe. The problem was to find a place to stay overnight. Luckily our club membership provides us with one complimentary room night at the hotel and much more.

So we used this opportunity to pamper ourselves, we took a day off, checked into the hotel, had spa and all meals in the hotel all for only INR 2000. Hotel Stay, SPA and breakfast was free and we just paid extra INR 2,000 for dining in the hotel 🙂

Our Room. picture: The Crown

Restaurant. picture: The Crown

Share with us in the comments how you hack luxury on a budget! We’ll keep sharing more of our hacks.

A positive attitude towards work is important for your happiness in life. However, working in a one-way-street fashion for others while ignoring your needs can make you unhappy at work. Get your life back using Early Retirement. In this article, I will share with you how my Early retirement journey has helped me be true to myself and perform better at my work. I hope it can help you to achieve happiness at work.

How you can get your life back using Early retirement

When you finish saving up a large corpus for early retirement as soon as possible you can leverage the bargaining power of your financial independence to make your job and your boss work for you as hard as you work for them. You will find yourself growing supremely confident even with just 5-7 years of expenses saved up. That’s what happened to me! Read on to know more..

My track record for negotiating a better job profile at my previous jobs was very poor because I would always settle for less than what I actually wanted.

The reason I could not negotiate better: I was solely dependent on my salary:

I had no cash-flow other than my salary. I was paying installments for my house. If my negotiation failed I couldn’t just quit the job. Also, finding another job requires you to upgrade your skills in your spare time after a whole day’s work since your day job is not giving you the exposure you need. Sometimes learning new skills is only possible by taking up a lower salary at the ground level of a startup or quitting your job to learn new skills or doing an MBA at your own time and expense. All of these options are not possible if you don’t have other income sources to tide you over for a few years especially when you have a family by now or loans to repay.

In short : Employers get that and have the upper hand as they know that you can’t just “up and leave” immediately even if you feel like it. You are more likely to “put up” with a bad situation since you think you have a “bird in hand”. All employers know this about their employees and that’s why employees don’t get a fair deal.

Working from a position of weakness is extremely damaging to your career, net-worth and self-worth:

My reluctance to negotiate hard for a fair outcome led to:

lower salary increments

career stagnation

working long hours project after project

not getting the exposure or bandwidth to learn new skills

visiting my aging parents only once a year

increase in stress and a decrease in health etc.

Ultimately I decided to achieve financial independence so I did not have to “put up” with employers who kept shortchanging me on money, skills, time and respect.

How my Early retirement journey helped me get my life back:

It has been 5 years since I left corporate life to start a business of my own working from home. In these 5 years working for myself, I’ve realized that I did not have a problem with working long and hard. In fact, I have more responsibilities now than when I was an employee only responsible for my work. I only had a problem with all-consuming jobs where only my employer’s needs were being met but my needs were not being adequately met. In the book Drive: The Surprising Truth About What Motivates Us , the author says that people are motivated by 3 needs beyond money :

If you are stuck in jobs that do not satisfy these 3 needs then I don’t blame you for dreaming about Early Retirement. Even though I did not plan it this way, I found to my pleasant surprise that growing my small business at my own pace has given me all of the above in addition to money and I’m happier as a result. I’ve never been more at peace with myself in a work setting before.

I live and work from Goa, the beach destination of India (Autonomy)

I set my own priorities for the business and how I get things done. (Autonomy)

I work from home so there is no commute and I set flexible work schedules including time for a quick power nap in the drowsy afternoons. At previous jobs, I had to fight the afternoon drowsiness with coffee & walks because you can’t be seen sleeping at your desk! (Autonomy)

I have time to learn new and difficult skills as they become necessary (Mastery)

Of course, the flip side is that I’m responsible 24x7x365 for customer support & tech issues even on weekends & vacations, unexpected deadlines, competitors, business growth, marketing, programming, etc. While all this was initially stressful for me as I only have a computer programming background, I have now accepted all this as part of learning how to run a better business. Also, this is making me more “Zen” about life in general since running a business has daily ups-and-downs like the stock market. So if you are in it for the long haul, you have to learn to reduce your stress and anxiety about short-term downturns. (Mastery)

The business is helping our family achieve financial independence so there’s purpose & meaning as well. (Purpose)

So overall I feel that I have a better work-life balance.

If I can make this lifestyle last for the rest of my life I would actually consider that to be early retirement! I got lucky but a large part of the luck happened because I had the staying power to go without making much money for the first 2-3 years in business as we had savings that would have lasted for 7 years. You too can create a lifestyle business if you save up a lot of money which is the point of early retirement I keep repeating through this blog. I could have been happier in my previous jobs as well if they had offered the same job satisfaction as my current lifestyle business.

“I had the staying power to go without making much money for the first 2-3 years in business as we had savings that would have lasted for 7 years”

3-Steps to F.I.R.E your bullshit job and F.I.R.E up for your Dream Job:

1. Start your journey towards F.I.R.E (Financial Independence & Retiring Early) to put yourself in a Position of Strength.

2. Once you become financially strong, negotiate confidently with your employer for what you want out of the job just like how employers expect you to constantly perform for them

3. Get them to respect your personal life, your need for keeping your skills up-to-date, desire to try different job roles and being paid adequately for the value you bring

If that’s not possible then you can quit immediately and take the time to find a better job instead of putting up with a job you hate or you can even start a lifestyle business. This way you never have to retire from working to find happiness!

After our Times Of India interview, I was interviewed about Early Retirement on Radio One Mumbai by the smart and talented RJ Annie of Radio One Mumbai 94.3 on the occasion of Worker’s Day (May 1). Coincidentally I had a blog post lined up on the same topic 🙂

Crisp Q&A. You’ll understand Early Retirement more deeply just by listening to this brief 7-minute interview.

Photos of our home, neighbourhood, travel and lots of home-cooked food… I don’t want to talk about money this time but let the pictures do the talking 🙂

Highlights:

We live in a place with good facilities for the general public which allows us to save as well as enjoy a comfortable lifestyle which I have showcased below.

All the cane furniture in our house was bought used from OLX and fixed up with varnish and repairs courtesy of my wife and her father.

Our swimming pool membership at a nearby 5-star hotel costs an affordable Rs.6000/year courtesy of my smart wife. The pool membership also comes with complimentary perks from their spa & restaurant.

The vacation photos are from Indian destinations 🙂

Hover over each photo to read the description for the photo

living room where we hang out

where we dine on our home-made food 🙂

World H.Q of this blog 🙂 my study overlooking a garden

walking path in nearby park

lawn in park for sitting or playing

our swimming pool at a nearby 5-star hotel

beach a drive away

home made grape wine

making mango wine at home

beach vacation

beach vacation panorama

riverside vacation stay

relaxing by the river

homemade pizza : we got all the recipes from online

home cooking : dhokla

breakfast : poha and chai

homemade idli and coconut chutney… perfect shapes 🙂

home cooking: pasta salad

home cooking : penne pasta

thai green curry ingredients basil, lemongrass, peri peri chilli etc

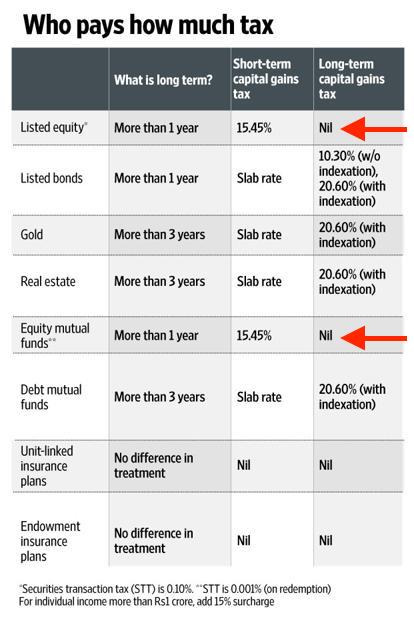

Starting with the recent budget , you have to pay 10.4%(including cess) long term capital gains tax (LTCG) on gains when you sell mutual funds or stocks after holding them for 1 year.

What does this mean for your Early Retirement plans?

Not the end of the world actually! If you are selling after holding for 25 years and your return was 12% then after paying LTCG tax your return falls to 11.54% : a negative impact of only 0.46%

Deepesh from personalfinanceplan.in has done a fantastic job of showing the impact of the tax on different CAGR % for corpus held over different lengths of time. I’m using an image from his article below:

As you can see above, the longer you hold, the lesser the impact of the tax which is perfect for the Early Retiree. For example: At 12% expected return, if you hold only for 5 years then the return falls to 10.99% due to tax but if you hold for 25 years the return only falls to 11.54%.

What Should You Do?

If you were expecting 12% returns from equity over 25 years then reduce your expectation to 11.54% and use the Early Retirement Excel calculator to calculate the increase in SIP required.

If you want to retire early at the same age as before this tax then you’ll have to increase the SIP amount. Just increase your SIP and don’t think any more about this tax.

Another very simple effect I very seldom see discussed either by investment managers or anybody else is the effect of taxes. If you’re going to buy something which compounds for 30 years at 15% per annum and you pay one 35% tax at the very end, the way that works out is that after taxes, you keep 13.3% per annum.

In contrast, if you bought the same investment, but had to pay taxes every year of 35% out of the 15% that you earned, then your return would be 15% minus 35% of 15%—or only 9.75% per year compounded. So the difference there is over 3.5%. And what 3.5% does to the numbers over long holding periods like 30 years is truly eye-opening. If you sit back for long, long stretches in great companies, you can get a huge edge from nothing but the way that income taxes work.

It will take us 1 extra year to achieve our Early Retirement target if we continue our current SIP amount. I’m actually relieved that the tax impact is only 1 extra year 🙂

Last month I posted that we had achieved 38% of our early retirement target. Our target is now reduced to 34% after factoring in LTCG. Remind me never to post a target achieved % before the government announces its budget 😉

This new tax only confirms my belief that to deal with Life’s uncertainties like this new tax you need to keep working and saving whatever you can even after reaching your target early retirement corpus. Today capital gains is set at 10%. Who knows, it may be raised to 30% over the next 25 years.

The biggest positive impact is that this new tax has validated our approach of letting our early retirement corpus compound for 25 years instead of trying to live off of the returns every year which would incur a 10% tax every year!! In our approach we would only pay a one-time tax of 10% at the end of 25 years. Re-read Charlie Munger’s statement above to understand what a big difference this makes.

Special thanks:

livemint : for first planting the doubt in my mind that I might be over-estimating the impact of this tax.

phreakv6 : for the Charlie Munger speech that pointed me in the exact direction

basuvinesh : for calculating the tax impact with a real example.

My wife : for giving me the simple idea to use Excel to calculate the exact post-tax CAGR % when I was trying to wrap my head around its impact on our unique early retirement plans which was not getting covered in the mainstream media.

deepesh raghaw : for the image I used earlier. his calculations matched my excel calculator including munger’s example so I’m confident of publishing this article and the excel 🙂 I especially agree with his quote below:

Fall from 10% p.a. to 9.49% p.a. may not look like much. However, when we talk about many years of compounding, the impact is going to be sizeable.

I have read accounts where many experts have mentioned that the impact is going to be minimal. That’s clearly not the case. Most of us shifted from regular to direct to save this extra 0.5-1% p.a. of the expense ratio. Didn’t we?

Therefore, let’s not fool ourselves. There is going to be an impact of LTCG taxation. Let’s accept it and pay the taxes happily.

This Valentine’s Day I want to touch on a touchy topic with couples : how to convince your significant other to work together as a team towards Early Retirement.

So this post has a guest section written by my wife on her experience getting convinced about early retirement.

Typically one person is super-excited after having read about Early Retirement online. But then they find that their partner is not as excited… atleast not that excited to single-mindedly focus on this goal to the exclusion of other goals in their life. Well.. you can’t forcibly convince someone to do something unless you want avoidable fights with your partner on this topic 🙂 You can however influence them positively. Influencing others requires that YOU be the change you want to see in others. So you need to lead by example.

MY WIFE’S STORY ON HOW SHE CAME ON BOARD:

While my husband was saving 50% of his monthly salary to pay instalments for his first house, I was busy spending most of my money on food, clothes, shoes and a high-flying lifestyle that I had discovered with my high-paying job. Saving money was not on the top of my mind. I was in a middle-management job at a start-up and everyone around me was exhausting their monthly credit card limits. Thankfully I never incurred debt and even paid for my car upfront with some help from my dad. But I did not save or invest seriously before the age of 30. That is when I got married, pooled our resources and made some lifestyle changes which reflected both our views on money.

The Aha! moment

In the beginning I used to find talking about my spending habits with my husband very difficult. I appreciated finer things in life and unfortunately they are not cheap. But after dozens of conversations with my husband I began to see that I associated Money with Quality of Life in the Present rather than as an Enabler to fulfill certain Life Goals in the Future. This meant that I was working a stressful, 12 hours a day job not having autonomy over my time in the present but also not securing my future. Being a single person I immersed myself long hours in work but I couldn’t imagine sustaining this once I had a family of my own with my husband.

I was valuing money over my time. And after our discussions my husband made me realise that I can control my time and then my life if I control “MY MONEY”. In the end I could not deny that the true role of money in my life was to serve me so I could live a happy, fulfilling life. I had to master my savings, my spending, and the investments so that I get the freedom I crave for.

In summary, I’m glad for this lifestyle that gives us more time to spend with each other and doing things that are important to us.

MY SIDE OF THE STORY:

My wife & I had different opinions about money when we got married. I wanted to retire early so I could move on to doing more meaningful work while also enjoying more leisure time. My wife saw money as a way to ensure a good quality of life where emotional needs were also fulfilled in addition to the physical needs.

Even before we got married, I used to talk finances with my wife for the post-married life. We even drew up a spreadsheet with our “ideal” lifestyle (ex: house with swimming pool, international travel etc). Since I was narrowly focused on saving as much as I could for early retirement, I used to overrule her idea of “quality of life” and focus only on the “bare basics” needed for sustenance like rent, food, insurance etc and strictly try to meet every month’s budget. At the same time I used to work long hours trying to maximise my earnings.

Naturally this approach caused friction & disagreements in the early days as we struggled to reconcile our two different approaches. For example: I remember once getting upset at the high prices in a gourmet store selling Thai food ingredients because my wife was planning to cook Thai that weekend. Ironically I did not realise that she was planning to cook at home towards my own goal of eating out less at restaurants.

To put it simply, I was being stingy instead of being frugal.

Slowly over the next 3 years we achieved a compromise between our approaches that was possible only because we loved & respected each other. I realised that aspiring for a good quality of life like my wife wanted had hidden benefits that cannot be quantified in money alone. For example:

Hiring a cook freed up time for me to exercise in the mornings. Earlier we cooked all meals ourselves.

When we moved from a 2BHK to a 3BHK rental I found the extra space more conducive to my work productivity since I work from home.

My wife also figured out that enjoying a higher quality of life did not always have to cost a lot. For example:

Instead of a house with a swimming pool she got us a swimming pool membership at a 5-star hotel nearby costing only Rs.6000 per year.

Instead of an international vacation she plans luxurious vacations at domestic destinations. We drive there by car saving on flight tickets which we splurge on the stay instead.

Right now we are at a happy balance where we try to achieve both our goals by saving as much as we can and living a life of quality while still staying within budget. I have added some suggestions below based on my learning from this process of give-and-take.

SUGGESTIONS BASED ON LESSONS LEARNED:

Lead by example.

Cut out the waste in your own life first : cigarettes, eating out, impulse purchases etc. Let them see you invest the savings. Follow this blog regularly for tips.

You don’t need your partner on board to get started. You go ahead first and let them follow at their own pace by watching you.

Find out what makes them tick.

Use that as a way in to influence them. My wife was motivated by freedom to pursue her interests as much as I was. She was not in any hurry to retire early but saw the benefits of savings which enabled her to quit her job for a few years to explore her interests. Having tasted freedom for a couple of years she indulged me in my early retirement plans so we could be free permanently.

In the case of MoneyMustache both him and his wife imagined being able to spend more time with their baby in the early years when the baby was growing fast.

This process of discovering what drives your partner is beneficial to your relationship as well because you will help your partner also achieve their dream.

Be willing to change yourself

As you can see above both my wife & I made changes to our attitudes to accommodate the dreams of the other person.

Your progress will be slow in the beginning but it will gain speed soon with two people working towards the same goal now.

If you are not willing to change yourself then you won’t have much success trying to convince your partner about early retirement.

Be Patient.

Don’t expect them to make drastic changes just because you had an overnight epiphany. Same goes for you. Don’t make drastic changes that you’ve not at-least given a week to think over to ensure that you can sustain it long-term.

Remember that it took us 3 years to get to our current happy equilibrium

Focus on Habits rather than results

These days I don’t micromanage & fret over my monthly expenses like I used to do in the early days.

We’ve incorporated many good habits like cooking at home, using the outdoors & internet for entertainment, saving up to buy only high-quality products etc that our monthly expenses stay within the budgeted range more or less.

So focus on the more difficult long-term behaviour change rather than the easy short-term results or exact budget numbers. It will take time but is more sustainable because neither of you will feel deprived of the good things in life.

Increase your income.

Target that promotion or change jobs. Sock away the extra income in SIP.

Show your portfolio to your partner every quarter to show the money growing.

Just make sure not to increase your expenses with the extra income. Easier said than done! but hey it is a valid suggestion 🙂

Inspire them.

Send them positive stories of others who have retired early.. make sure that the role-model appeals to your partner’s aspirations & goals in life. Some role-models below:

% Saved for Early Retirement : 38% 34% (target % reduced due to 10.4% LTCG tax announced in the budget after this post was originally published. I’ll write a detailed article on this new tax’s impact next month)

Next year we are hoping to reach 50% 46% of our target. Fingers crossed!

I’ll update the progress bar on the right-hand sidebar every year with our progress

Current Monthly Saving rate : 25%

single-income household as mentioned in the NRI post.

this savings is from my business income

Effective Monthly Saving rate : 50%

wife is moving her low-return F.Ds to mutual funds via SIP so we are effectively saving 50% of income in mutual funds towards retirement.

We currently have a 60:40 split between active Mutual Funds & inactive EPF/PPF.

more SIP in the coming years will tilt this balance towards equity

Our Total Portfolio Return is approximately 14%. OurExpected return is lower at 12%.

Our Large-Cap fund returned 18% as of Dec 2017. We are taking this as indicative of our equity returns even though we have some mid-caps that performed better because only our large cap fund shows the XIRR 🙂 For accurate numbers we have to calculate manually and we haven’t done that yet.

Our PPF interest rate was 7.6% as of Dec 2017. Using this as indicative of debt returns. I’m deliberately using the lowest PPF rate since I’m approximating here.

So with a equity:debt ratio of 60:40, our total portfolio return is around 14%. (60×18% + 40×7.6%)

I’m sharing our returns only to document the numbers so we can look back many years from now on the ups-and-downs in returns. We are not really worried about the ups-and-downs as it will get smoothed out over the years like I explain in my blog post 12% return from stock market every year?

I mention that I was an NRI in the Disclosure of this blog but I wanted to address this issue head-on because of a recent comment in JagoInvestor where someone said only NRIs can save a lot in a short time which is a false statement and only serves as an excuse for the self-pity crowd.

Here’s my brief NRI story:

I worked and earned in the U.S for about 9 years. I returned to India in 2013.

But before you go “oh! that’s how you saved so much so quickly”, my U.S salary was not really high. I started with a really low salary and since increments are based on your previous salary … my salary grew very slowly especially when I was a startup employee for 6 years.

Note that as of this time, we’ve saved up only 30% of our early retirement target. See the progress bar on the right hand side. This 30% includes my wife’s savings also. I’m now in India. This means that I’ll be saving the remaining 70% of our early retirement target working from India. My wife is currently on a break from work to explore her interests meaning we are a single-income household for the past 3 years. So I’ll be demonstrating how early retirement is possible in India by my personal example in the years to come!

My NRI salary was only good enough to buy a Rs.45 lakh apartment over 5 years without requiring any home loan. This works out to an average savings of Rs.75,000 per month for 5 years. (Rs.45 lakhs divided by 5 years). Given the real-estate crash in India right now, the apartment is now worth about Rs.65 lakhs after 9 years since I booked it in 2008 which is a terribly low CAGR return of only 4%! I would have invested that amount in mutual funds instead if I had educated myself. The first 3-4 years of my NRI stint, I was paying off my education loan and large credit card debt I had gotten into due to poor financial habits.

I was always embarrassed that I did not earn the big salaries of my peers in the same age group. But as I write this disclosure I’m glad I didn’t because I learned to save instead to achieve my goals and not succumb to increased lifestyle expenses with increasing salary 😉 Moreover it is my U.S experience that helps me apply Early Retirement ideas from the U.S to Indian conditions.

I grappled with the dilemma of whether to mention that I had been an NRI at the time of writing the Early Retirement article and finally decided not to mention it so that readers were not distracted from the main message of saving at-least 50% of your salary each month. From the comments on the article I can now say that my decision was correct because no one complained it was not possible to save 50% on an Indian salary. Because people were already saving 50% of their Indian salary as EMI to repay house loan just not as mutual fund SIP like I was advocating.

Coming back to this self-pity comment : recently on JagoInvestor an NRI had written an inspirational article how they had saved Rs.1.5 crores in just 7 years by investing aggressively in equity and not buying real-estate. But this commenter dismissed the achievement by saying only NRIs can do it and people in India should keep saving till age 60. I posted a reply to their comment showing how people on an Indian salary can also save the same amount in just 7 years.

My reply to the self-pity comment saying only NRIs can save a lot in a few years:

1. You should compare this NRI author with a double-income household working in IT in bengaluru/pune where husband and wife each bring in Rs.1 lakh/month. I know Indian households where one spouse’s salary is used for house loan EMI and the other spouse’s salary for expenses. If this double-income couple saved Rs.75,000/month in mutual funds then @ 12% CAGR they would have Rs.1 crore saved in the same 7 years as this NRI. That is compounding & equity returns at work.

2. If households in India can afford to pay EMI of Rs.75,000 per month on a Rs.75 lakh house loan then they can invest the same amount each month in equity too. Most people in India are saving a lot each month but in the wrong manner as EMI which this NRI smartly avoided.

3. You say people in India don’t earn that much.

But I’ve recently hired IT people in Pune & Bengaluru with minimum take-home pay of Rs.1 lakh/month for 5-7 years experience. That’s when I realized that such high salaries are the norm in Pune, Bengaluru etc. You have to agree that the past decade or so has been lucrative for IT and MBA people working in India.

4. Quite a bit of people reading this blog are high-earners early in their careers in IT, MBA etc

It is possible for them working with their spouses as a team to emulate this NRI’s impressive achievement.

5. Lastly, you are discounting the fact that cost of living is also high for NRIs as it is denominated in their foreign currency. So unless you are consistently frugal, you won’t be able to save much. What is impressive about the author is that he has consistently saved for 7-9 years which requires determination.

I will definitely consider this as the “inspiration story of the decade” for young people entering the workforce

We need inspirational stories like this because IT & MBA jobs are no longer secure that you can hope to work till age 60.

I’m recovering from a lengthy and painful throat infection this new year. So I thought it would be apt to start 2018 with this topic. All of 2017 I took pride in never taking a single pill except a painkiller for a dental issue. I finally took some Ayurvedic pills for this infection after realising that this infection might be serious.

YOU MISS HEALTH ONLY WHEN YOU DON’T HAVE IT:

I obsessively talk a lot about money but all the money in the world means nothing if you don’t have the health enjoy it. Like I mentioned in the Early Retirement article, my wife & I do Health SIP in some simple ways : yoga, nutritious food, morning walks, swims etc. I used to cycle & play badminton a few years back and I would love to get back to both activities.

DIABETES – A LIFESTYLE DISEASE:

Personally my need for Health SIP comes from the fact that both my parents are diabetics and I can see how their quality of daily life is reduced in old age, so I’m obsessed with avoiding diabetes as much as I can through healthy living. My mother tells me they used to call diabetes “the silent killer” because people would know someone had diabetes only after they died. On the surface the person who died would look healthy but diabetes was corroding organs inside.

If you want to avoid major health expenses in your old age then you need to start paying attention to your:

DIET

EXERCISE

STRESS

The conventional approach to retirement is to earn the maximum and save the maximum because you never know how much you need… coz you might get diabetes and diabetes treatment is expensive etc etc. But we forget that eating out every day because we are at work, skipping exercise because we work long hours and not dealing with work stress means that it will all catch up as you get closer to old age and will be very expensive to treat not to mention your quality of life will be so poor you can’t even climb stairs easily or travel to visit your children etc. So the solution is to lead a balanced life.

We are trying a different approach inspired by moneymustache’s badass approach. We already see the oldies in our family and what kind of problems they face.

For example:

Elderly ladies always have knee problems from standing in the kitchen for long hours every day cooking for the family 3 meals a day

Elderly men have diabetes from having a “desk job” and not exercising enough

Liver problems from alcohol abuse

Antibiotic resistance : needing higher dosage of western medicine as a result of popping pills indiscriminately …Fever? take a Crocin, Headache? take Saridon etc . Would it have killed to let the fever go away on its own in 5 days? The body would have developed better immunity that way.

OUR HOLISTIC WELLNESS PLAN:

So our plan is to avoid atleast what we can see the oldies suffering from . And then prepare for some of the issues our generation is likely to get like

Poor eyesight from starting at phone & computer screens for too long

Diabetes from junk food, no exercise and work stress

Alcohol abuse as social drinking becomes more mainstream

Heart problems from working in stressful work environments or not dealing with personal life stress via meditation, exercise, better communication etc.

Here are some simple changes we’ve made to our diet, exercise and stress-management.

DIET:

Home-cooked food & eating out less but in high quality places.

Moderate Alcohol for social occasions.

Disclosure: we have a cook who comes home and makes us home-cooked food. The benefits far outweigh the costs.

EXERCISE:

Swimming

Walks

Yoga

STRESS MANAGEMENT:

Meditation

Improving communication with spouse.

Not habitually checking on work after work-hours.

Starting now, I urge you to make small & simple changes to your diet, exercise and stress-levels.Trust me you’ll save a ton of money staying healthy.

Around me I see super-active and healthy 80-year olds and very-unhealthy and tired 60-year olds. How old you “feel” is a matter of how healthy you are. Please start taking care of your health atleast now before it is too late.

You’ve heard the saying “The Rich Get Richer”. It is usually uttered in a negative manner to hint that only the rich get richer and the rest only get poorer. In this blog we do not pull other people down for their successes. Instead we try to learn from others who’ve done well and apply it to improve our life.

Source: Quickmemes

An Early Retiree is also a “Rich” person who has accumulated a lot of capital by aggressively saving their salary for 10-15 years. So let’s try to understand how “The Early Retiree Can Get Richer” by listing out the many ways in which the Rich use their accumulated capital to their advantage.

You can implement some of these strategies even now before fully accumulating your retirement corpus.

Table of Contents:

The Early Retiree pays no interest for loans